02 / How It Works

Four-agent pipeline

Every weekday at 10:35am GMT, thirty minutes after London open, once the opening noise has settled, the system runs. No human input. APScheduler fires five jobs throughout the day. Nothing is held overnight.

10:30

Start candle collection via Lightstreamer

10:35

Full 4-agent evaluation scan

12:00

Regime recheck: close if FTSE <-1%

14:00

Second regime recheck

16:00

Liquidate everything, nothing overnight

Kill-Switch

Check equity floor (£750)

Market Regime

FTSE down >0.5%? Skip session

Parallel Scan

20 tickers + RNS news (Tier A/B/C)

Technical Indicators

EMA-50 + VWAP + RSI-14

Claude Quality Gate

Sonnet rates setup 1--5

Claude Risk Audit

Opus approves or vetoes

Execute or Kill

SL 3% / TP 6% / max 1 position

16:00 Liquidation

Nothing held overnight

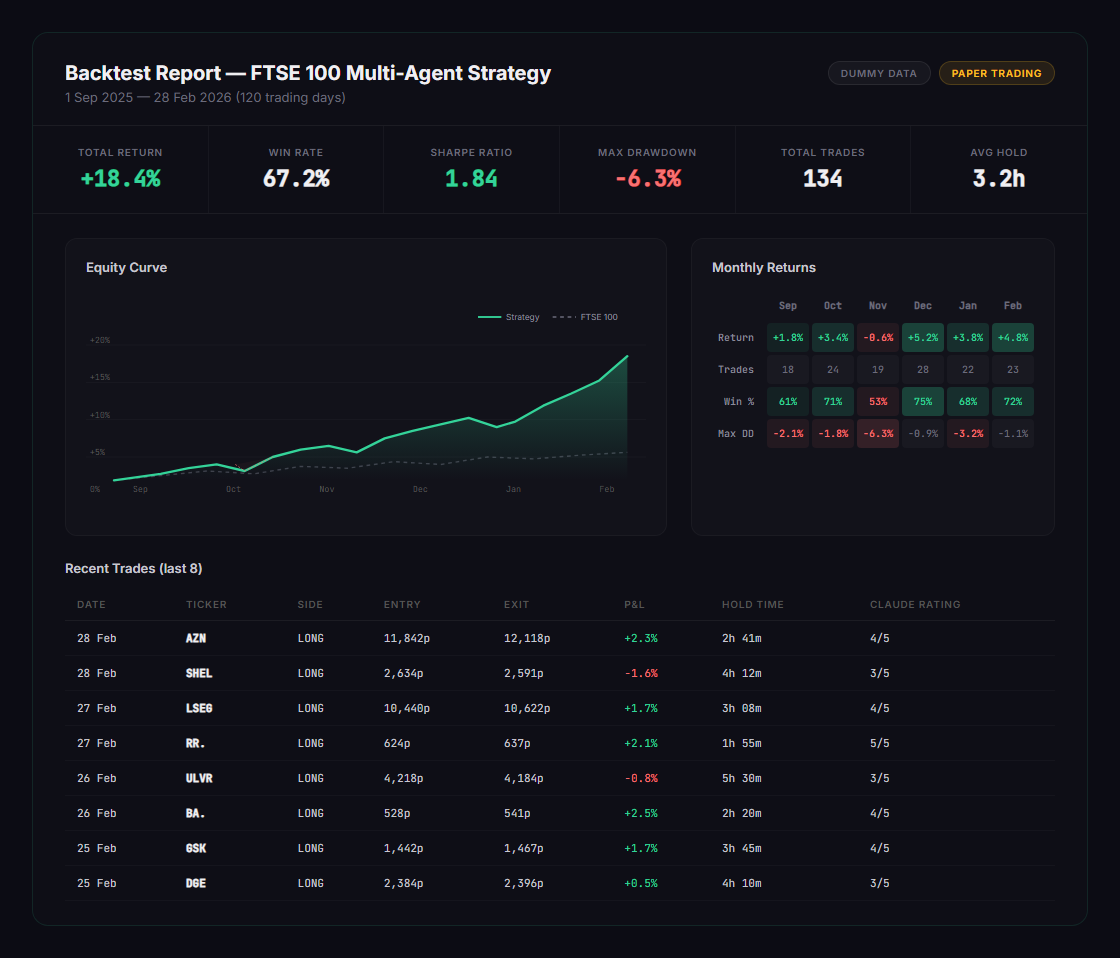

trading-bot : scan output

10:35:01 SCAN Kill-switch OK: equity £2,847

10:35:02 SCAN FTSE 100: +0.12%, session active

10:35:04 PASS AZN: EMA OK, VWAP OK, RSI 42

10:35:04 SKIP SHEL: RSI 78 (overbought)

10:35:04 SKIP ULVR: below EMA-50

10:35:05 CLAUDE AZN rated 4/5, clean setup

10:35:06 AUDIT Opus approved, low correlation risk

10:35:07 EXEC BUY AZN @ 11,842p | SL 11,487 / TP 12,553

First thing every morning: kill-switch and market regime check. If either fails, nothing else runs. RNS news gets scanned via Claude web search, headlines classified as Tier A (earnings, M&A), B (buybacks, upgrades), or C (skip). This replaced a BeautifulSoup scraper that kept breaking. Then the technical check: EMA-50, VWAP, RSI. Only stocks that pass get sent to Claude Sonnet for a quality rating, strict JSON schema, no fallback. Last step is Claude Opus as risk auditor. The hard rails live in code, not prompts: £750 max notional, one position at a time, equity above floor. If Opus vetoes, the trade dies. Running paper-trade on a demo account while I wait for enough data to trust it.